Mortgage Investment Corporation Can Be Fun For Everyone

Table of Contents7 Simple Techniques For Mortgage Investment CorporationMortgage Investment Corporation Fundamentals ExplainedThe Main Principles Of Mortgage Investment Corporation Mortgage Investment Corporation - QuestionsMortgage Investment Corporation Can Be Fun For Everyone

Does the MICs credit scores board evaluation each home mortgage? In a lot of circumstances, home loan brokers manage MICs. The broker should not act as a participant of the credit score committee, as this places him/her in a straight dispute of passion given that brokers normally make a commission for putting the home mortgages.Is the MIC levered? The financial institution will certainly approve particular home mortgages had by the MIC as protection for a line of credit scores.

This must attend to additional scrutiny of each home loan. 5. Can I have copies of audited financial declarations? It is very important that an accountant conversant with MICs prepare these statements. Audit treatments need to guarantee stringent adherence to the policies stated in the information package. Thank you Mr. Shewan & Mr.

The Only Guide for Mortgage Investment Corporation

Last upgraded: Nov. 14, 2018 Couple of financial investments are as beneficial as a Home loan Financial Investment Corporation (MIC), when it involves returns and tax benefits. Due to their business framework, MICs do not pay earnings tax and are lawfully mandated to disperse all of their incomes to financiers. MIC returns payments are dealt with as passion earnings for tax obligation objectives.

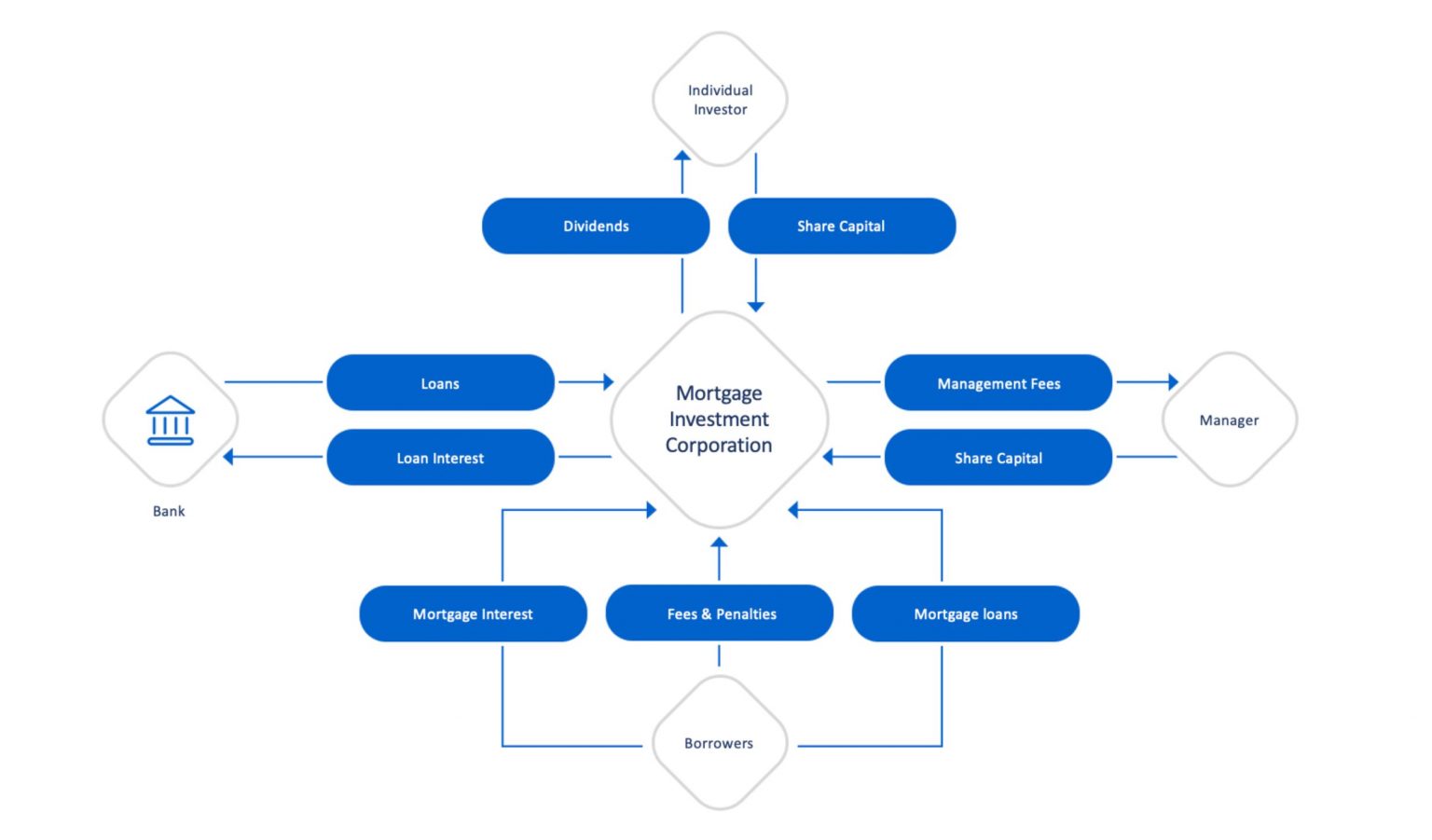

This does not imply there are not threats, however, generally talking, no issue what the wider stock exchange is doing, the Canadian realty market, specifically major urbane areas like Toronto, Vancouver, and Montreal does well. A MIC is a corporation created under the rules establish out in the Revenue Tax Obligation Act, Section 130.1.

The MIC makes income from those mortgages on rate of interest fees and general charges. The genuine charm of a Home loan Financial Investment Firm is the return it supplies capitalists compared to other fixed revenue financial investments. You will certainly have no difficulty discovering a GIC that pays 2% for a 1 year term, as government bonds are equally as low.

The 45-Second Trick For Mortgage Investment Corporation

There are strict demands under the Income Tax Obligation Act that a corporation must fulfill prior to it certifies as a MIC. A MIC has to be a Canadian corporation and it need to invest its funds in home mortgages. In truth, MICs are not allowed to manage or establish realty property. That claimed, there are times when the MIC ends up possessing the mortgaged residential property because of foreclosure, sale contract, etc.

A MIC will earn interest income from home mortgages and any money the MIC has in the financial institution. As long as 100% of the profits/dividends are offered to investors, the MIC does not pay any revenue tax. Rather of the MIC paying tax on the interest it earns, shareholders are accountable for any additional info kind of tax.

10 Easy Facts About Mortgage Investment Corporation Shown

And Deferred Plans do not pay any type of tax on the passion they are approximated to obtain - Mortgage Investment Corporation. That claimed, those that hold TFSAs and annuitants of RRSPs or recommended you read RRIFs might click this site be struck with certain fine taxes if the investment in the MIC is considered to be a "restricted financial investment" according to Canada's tax obligation code

They will ensure you have found a Mortgage Financial investment Company with "certified financial investment" standing. If the MIC qualifies, maybe really beneficial come tax obligation time since the MIC does not pay tax on the rate of interest earnings and neither does the Deferred Plan. Extra generally, if the MIC fails to meet the demands established out by the Income Tax Act, the MICs revenue will be tired prior to it obtains distributed to shareholders, reducing returns substantially.

It appears both the actual estate and securities market in Canada are at all time highs Meanwhile returns on bonds and GICs are still near record lows. Even cash is losing its charm since power and food rates have pressed the rising cost of living price to a multi-year high. Which begs the concern: Where can we still locate worth? Well I believe I have the answer! In May I blogged about checking into mortgage financial investment companies.

The Facts About Mortgage Investment Corporation Uncovered

Numerous effort Canadians that wish to acquire a house can not get home mortgages from traditional financial institutions since probably they're self employed, or do not have a well-known credit report yet. Or maybe they desire a short-term financing to create a big home or make some renovations. Financial institutions often tend to disregard these potential consumers because self used Canadians don't have stable revenues.